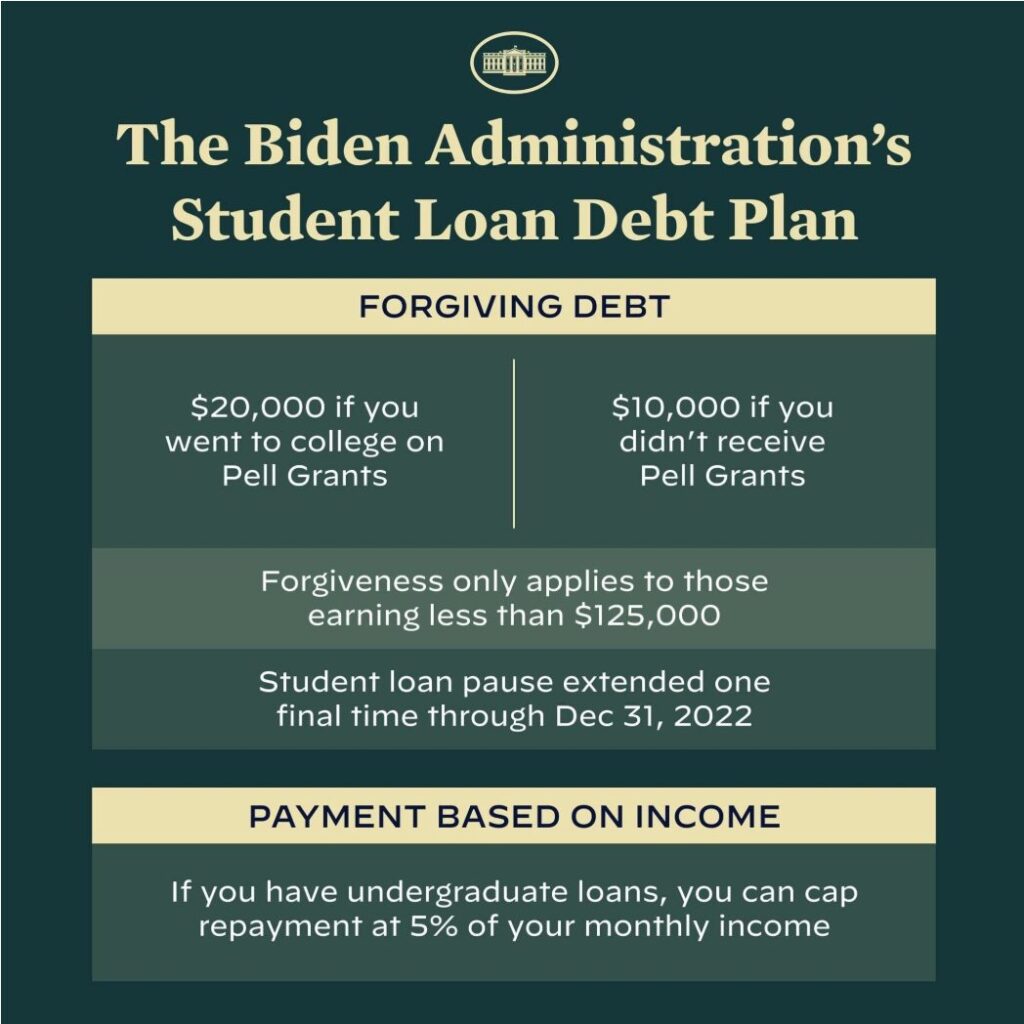

Last year it was reported that roughly 13% of Americans are currently dealing with student loan debt. That’s one in every eight people. That means that even if you manage your student loans well, you are still directly affected by the ever changing federal policies and procedures. In an October press release, President Joe Biden said, “From day one of my administration, I promised to fight to ensure higher education is a ticket to the middle class, not a barrier to opportunity.” And since taking office in 2020, that’s exactly what he’s done. The Biden/Harris administration made student loan debt relief a high priority, enduring numerous challenges and court battles trying to convince conservative judges across the country that Americans DESERVE paths to financial freedom not only because they worked hard for it, but also because it is a key factor needed to participate in and contribute to a successful and thriving economy. There’s a lot that has been done, and a lot that is being done, and sometimes the information can be so overwhelming to the point where the average American student loan borrower doesn’t even know if they’re eligible, or how to navigate the process to find out.

Federal student debts may be discharged, canceled, or forgiven under specific circumstances. The definitions of “forgiveness,” “cancellation,” and “discharge” are nearly identical, all implying that you won’t be required to repay all or part of your student loan. The most popular avenue for student loan forgiveness is Public Service Loan Forgiveness, although there are many other paths to decreasing and eliminating federal education debt. For instance, if you are a teacher, a government employee, nurse, doctor, or other medical professional you could be eligible for loan forgiveness. If you work for a nonprofit, have a disability, are a parent borrower or a Perkins Loan Borrower, have declared bankruptcy, or repay your loans under an IDR (Income Driven Repayment Plan) you too could qualify you for federal student loan assistance. There are also special circumstances for student loan discharge by death, school closure, forgery, and/or proof of being misled by an academic institution.

There have been several student loan forgiveness programs, some have expired, some are still existing, and some are being held up in court. They include:

The HEROES (new plan, overturned in court)

The Higher Education Act Part 1 and 2 (new plan—forthcoming, partially paused by courts)

SAVE (new plan, paused by the courts)

The Student Loan Payment Pause (Existing and extended plan, now expired)

The Public Service Loan Forgiveness Plan (Existing and extended plan, still active)

The Borrower Defense to Repayment (Existing and extended plan, still active, though recent changes are paused during a court case)

The Closed School Discharge (Existing and extended plan, still active though recent changes are paused during a court case)

The Total and Permanent Disability Discharge (Existing and extended plan, active)

Waiving Interest

There are many people who are weary about the upcoming return of the Trump administration and how that will affect paths to Student Loan Forgiveness under his previous threats of wanting to eliminate the Federal Department of Education, but if you want to find out more information about these programs and check your eligibility, you can still visit the Department of Education’s website, as well as the website for Federal Student Aid.

When it comes to student loan forgiveness, the Biden administration has proved to be the most proactive in history. The administration has canceled a significant amount of debt ($180 billion and counting) in spite of numerous obstacles. Although many of its initiatives to forgive student loans have been unsuccessful, there are still numerous active strategies in place, and more are anticipated throughout the remaining days of the Biden administration, with the hopes of securing their place in federal legislation.

{kind=link}